Good morning. Nvidia stock closed 10 per cent off its recent peak yesterday, despite a steady flow of news about all the life-changing AI models just around the bend. Unhedged has two very simple tests for assessing AI efficacy. First, can it file our expenses? At that threshold, it is productivity-enhancing and good. Second, can it replace us? Then, it is productivity-destroying and must be stopped at all costs. Email us: robert.armstrong@ft.com and ethan.wu@ft.com.

How much inflation is priced in?

More and more market participants and pundits are betting that stalling disinflation might stop the Federal Reserve from cutting rates at all in 2024. The past two months of inflation reports have been too hot, and recent Fedspeak has sounded a touch hawkish. For months, markets have been ratcheting back rate-cut expectations. Now, the market-implied year-end rate exceeds the Fed’s latest rate projections. Might the gap widen?

On Wednesday we’ll see fresh consumer price inflation data, which could make the hot January and February reports seem like the anomalies many experts insist that they are. If not, it will look a lot like inflation has stagnated around 3 per cent. Economic growth looks strong. Nominal wage growth is around 4-5 per cent, a level historically inconsistent with 2 per cent inflation. This week’s data on consumer inflation expectations, which the Fed sees as fundamental to inflation, wasn’t encouraging. Expectations picked up on a three-year horizon, rising to 2.9 per cent from 2.7. One-year-ahead inflation expectations have fallen sharply in the past year, but since December they’ve been stuck at 3 per cent.

With growth as strong as it is, there is a deepening consensus that the most likely economic outcome is “high-for-long soft landing”, as JPMorgan’s Marko Kolanovic put it in a note out Tuesday.

How easily would markets digest stubborn inflation, resilient growth and high rates? To get a sense, we had a look at how much inflation is priced in. Backing near-term inflation expectations out of market prices isn’t straightforward. You have to take a wide survey and make a best guess.

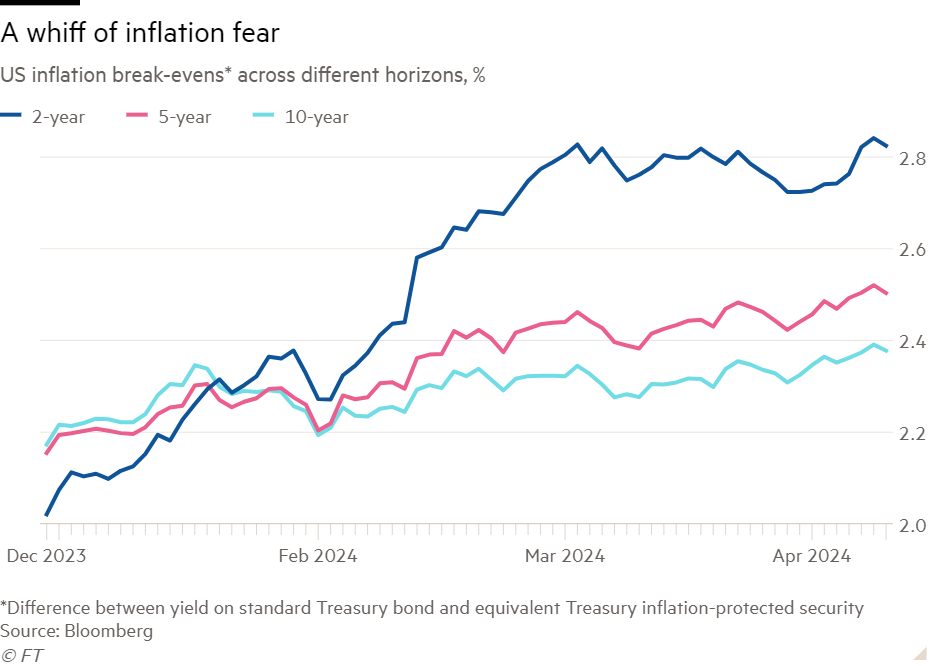

The most striking recent development is in the inflation-linked bonds market. Two-year inflation break-evens (the yield on vanilla Treasuries less the yield on inflation-indexed ones, also called Tips) began the year at 2 per cent, but have shot up to 2.8 per cent. This measure is based on the two-year Tips market, which is thin and must be taken with a grain of salt. But more reliable longer-term break-evens are rising too:

This looks to us like caution, not panic. Inflation break-evens are indexed to US CPI, rather than the personal consumption expenditure price index that the Fed targets. This matters because of the historical “wedge” between CPI and PCE inflation. Over the past three decades, headline CPI inflation has averaged around 40bp higher than PCE. So CPI hovering at 2.5 per cent, as the five-year break-even suggests, would almost be consistent with the Fed’s 2 per cent PCE inflation target. Near-term nerves, long-term confidence.

A similarly cautious note is apparent in the futures market. The modal outcome this year is still cuts; currently, three are priced in. But other scenarios are looking more likely. According to the Atlanta Fed’s rates-market tracker, since February the probability of no cuts in 2024 has doubled, to 10 per cent. The chance of a rate rise this year has risen, too, from 5 per cent in February to 8 per cent now. These are still tail risks, but the tails are getting fatter.

Interestingly, the inflation swaps market has been relatively quiet. The five-year/five-year forward rate, which measures market-expected inflation over the five-year period beginning five years from today, has only ticked up a little. The 5y/5y started 2024 at 2.5 per cent, in line with its 20-year average. Today, it’s at 2.6 per cent.

In stocks and commodities, you can also turn up evidence of inflation risk being priced in. The chart below shows several plausibly inflation-sensitive assets. The last one, in blue, is an actively managed inflation-hedging ETF that combines exposure to inflation-linked bonds, commodities, real estate and resource extraction stocks. It has bounced since February:

This is circumstantial evidence. The recent oil price increase is as much about geopolitics as firm global demand, gold’s rally is baffling analysts and industrial metals are being supported by recovering Chinese demand. But on the margin, it adds to the case that inflation nerves are creeping in.

All told, this is a picture of markets that are more calm than panicked, but which are awake to the still-present inflation risks. (Ethan Wu)

Replies on private equity excess returns

Yesterday’s piece about excess returns in private credit drew a lot of meaty responses from readers, from all sides of the debate.

Edward Finley of Arrow Wealth Advisory LLC pointed out that from a certain point of view, the question “does private credit, as an asset class, generate excess return” is a sort of category mistake:

An asset class (properly understood) is a collection of systematic risks. By definition, that’s not something that should earn any returns in excess of its systematic risks . . . It would be odd for anyone to show that the average high- yield fund does not earn returns in excess of its risks, and think that they have proven anything useful.

There is something to this. Understanding excess returns as added returns that do not come with added risk, they should not be a feature of an asset class in an even moderately efficient market. It’s a free lunch, and in a functional market, either the lunch stops being free, or it all gets eaten.

Most of the people who said there was excess return to be harvested argued, in one form or another, that those returns were functions of frictions in lending markets, frictions private credit funds could charge borrowers for removing.

Here, for example, is Marco Hanig, CEO of Alternative Fund Advisors:

The key reason for excess returns is the “sourcing premium” . . . neither retail nor institutional investors can invest directly in a private loan. The loan has to be originated, covenants negotiated, creditworthiness established — basically all the activities that banks used to do (and to some extent still do) before tighter regulations, capital requirements, etc created a lending vacuum. The private credit premium is simply compensation for doing all this work — “economic rent” in economist jargon.

Hanig notes that the premium is larger for smaller loans. For half-billion-dollar loans where the likes of Apollo, Ares and KKR bid, he doubts whether there are excess returns to be had.

C Shawn Booking agrees that private credit funds

earn higher spreads and total yields because they’re providing speed, certainty of execution and cost of capital; privacy in terms of the borrower not needing to become a public filer; an ability to [do] deep-dive diligence and finance complex situations that aren’t suitable to the vanilla, diligence-light public syndicated markets; structuring creativity; an ongoing financing partnership that means sponsors and management teams can quickly and readily tap into follow-on financing . . . a de facto insurance policy in a downside scenario in that the sponsor / borrower can have a rational, constructive negotiation . . . without losing their company to a herd of brawling cats in the form of distressed investors

Paul O’Brien placed the friction firmly on the side of the banks:

Bank credit is artificially expensive because of regulations like capital and leverage rules. We do this to limit risk to the deposit base. So, when bank lending dominates credit markets, unregulated private capital can earn an excess return.

But, he points out, the free lunch will be eaten:

This should not be a permanent situation. As we are seeing now, more private capital will flow in, banks will step back, and the excess returns will fade. They probably have [already].

Recall that the authors of the recent paper arguing that private credit investors do not receive any return in excess of risk — Isil Erel, Thomas Flanagan and Michael Weisbach — agree that this form of economic rent exists, but at an aggregate industry level gets eaten up by fees:

The return that [private credit] borrowers pay in excess of the risk-adjusted interest rate approximately equals the fees that the private debt funds charge. Rents earned by the funds from making private direct loans accrue to the general partners, not the limited partners. They appear to reflect compensation for identifying, negotiating, and monitoring private loans to firms that could not otherwise raise financing.

It seems that most people agree, then, on the source of the excess return. The debate is whether it will persist as the industry attracts more capital, and whether it exceeds the fund fees. Here’s Hanig again, taking the other side of the argument from Erel, Flanagan and Weisbach:

The final open question is whether the private credit managers keep the economic rent for themselves through high fees. I can tell you from first-hand experience that (especially at the small-cap end) they take their pound of flesh, but there’s plenty left over for investors.

One good read

A defence of the more-abortion-means-falling-crime theory.

FT Unhedged podcast

Can’t get enough of Unhedged? Listen to our new podcast, hosted by Ethan Wu and Katie Martin, for a 15-minute dive into the latest markets news and financial headlines, twice a week. Catch up on past editions of the newsletter here.

Read More: World News | Entertainment News | Celeb News

FT